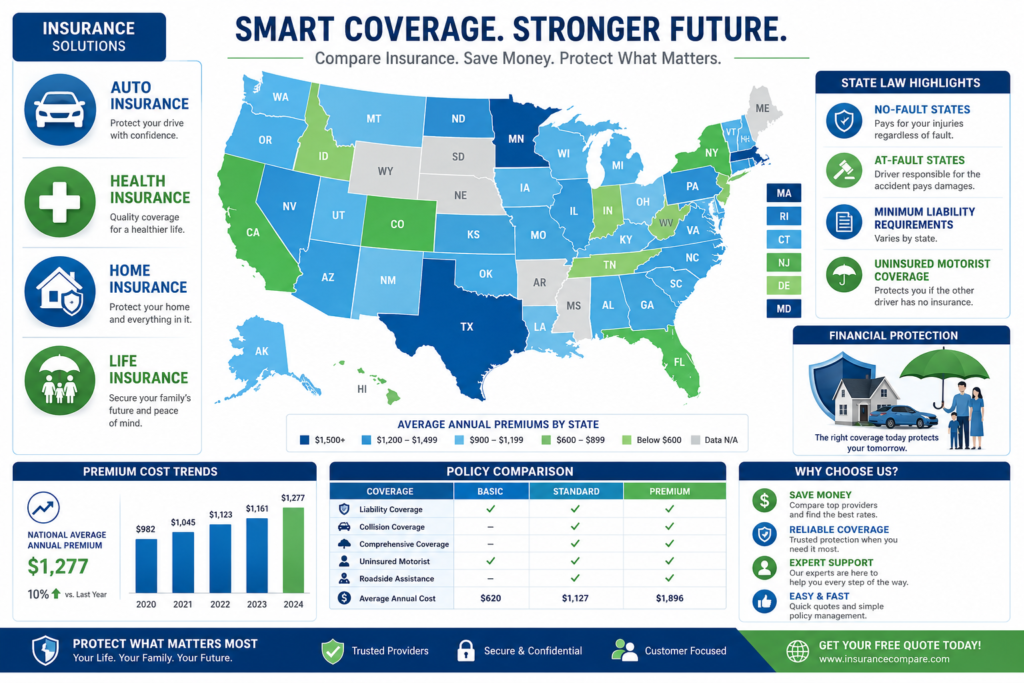

Understanding Insurance Costs and Coverage Across the United States

Insurance is one of the most important financial tools for protecting your assets, health, family, and future. However, insurance regulations, coverage requirements, and premium costs vary significantly from state to state. Whether you’re shopping for auto insurance, health insurance, homeowners insurance, or life insurance, understanding your state’s unique laws and market conditions can help you make smarter decisions and potentially save thousands of dollars.

This comprehensive state-by-state insurance guide explains how insurance plans differ across America, what legal requirements consumers should know, and the real-world costs that affect insurance premiums.

Why Insurance Costs Vary by State

Many consumers are surprised to discover that identical insurance policies can cost dramatically different amounts depending on where they live. Several factors contribute to these differences:

State Regulations

Each state regulates insurance through its own insurance department. These agencies establish rules regarding:

- Minimum coverage requirements

- Consumer protection laws

- Claims handling procedures

- Rate approval processes

- Licensing standards

States with stricter regulations may offer stronger consumer protections but can sometimes experience higher premiums.

Local Risk Factors

Insurance companies calculate premiums based on local risks such as:

- Traffic density

- Accident frequency

- Weather-related disasters

- Crime rates

- Healthcare costs

- Property values

For example, coastal states prone to hurricanes often experience higher home insurance premiums, while states with dense urban populations may have more expensive auto insurance rates.

Economic Conditions

Medical costs, construction expenses, labor rates, and litigation trends also influence insurance pricing throughout the country.

Auto Insurance by State

Minimum Auto Insurance Requirements

Nearly every state requires drivers to carry some form of auto insurance. However, required coverage limits vary considerably.

Most states mandate:

- Bodily injury liability coverage

- Property damage liability coverage

Some states additionally require:

- Personal Injury Protection (PIP)

- Uninsured motorist coverage

- Medical payments coverage

For example:

- Florida requires Personal Injury Protection coverage.

- California has liability insurance requirements but no PIP requirement.

- New York requires both liability and uninsured motorist protection.

Understanding your state’s minimum requirements is essential because driving without proper insurance can result in fines, license suspension, and legal penalties.

Average Auto Insurance Costs

Auto insurance premiums vary dramatically nationwide.

Generally:

- High-cost states often include Florida, Louisiana, Michigan, and New York.

- Lower-cost states often include Idaho, Vermont, Maine, and Ohio.

Factors affecting premiums include:

- Driving record

- Vehicle type

- Credit score (where permitted)

- Age and experience

- ZIP code

- Annual mileage

Drivers should compare multiple quotes annually because rates can differ significantly among insurers.

How to Save on Auto Insurance

Consumers can often reduce premiums by:

- Bundling policies

- Maintaining a clean driving record

- Increasing deductibles

- Taking defensive driving courses

- Utilizing telematics programs

- Shopping for quotes regularly

Health Insurance by State

State Health Insurance Markets

Health insurance is regulated at both federal and state levels. While federal laws establish baseline protections, states maintain significant authority over insurance markets.

State differences may include:

- Marketplace plan availability

- Medicaid eligibility

- Consumer protections

- Network requirements

- Coverage mandates

Residents should review their state’s healthcare marketplace during open enrollment periods to compare available plans.

Average Health Insurance Costs

Health insurance premiums vary significantly based on:

- State of residence

- Age

- Family size

- Tobacco use

- Coverage level

States with higher healthcare costs generally experience higher insurance premiums.

Consumers should evaluate:

- Monthly premiums

- Deductibles

- Copayments

- Coinsurance

- Out-of-pocket maximums

The cheapest plan may not always provide the best overall value if medical needs are substantial.

Medicaid Expansion and State Differences

Many states have expanded Medicaid eligibility, increasing access to affordable healthcare coverage.

However, eligibility requirements and enrollment processes differ by state. Consumers should check local guidelines to determine whether they qualify for financial assistance programs.

Home Insurance by State

Why Home Insurance Costs Differ

Homeowners insurance rates are heavily influenced by geography.

Major risk factors include:

Natural Disasters

States prone to:

- Hurricanes

- Wildfires

- Tornadoes

- Flooding

- Earthquakes

often face significantly higher insurance premiums.

Property Values

Higher home values increase replacement costs, leading to more expensive coverage requirements.

Construction Costs

Labor shortages and rising material costs affect rebuilding expenses and insurance rates.

States with Higher Home Insurance Costs

States frequently experiencing severe weather events often rank among the most expensive for homeowners insurance.

Examples include:

- Florida

- Louisiana

- Texas

- Oklahoma

Insurance carriers continually adjust rates based on claims history and catastrophe modeling.

States with Lower Home Insurance Costs

States with fewer natural disaster risks often offer lower premiums.

Examples may include:

- Vermont

- Delaware

- Idaho

- Oregon

However, local market conditions still influence pricing.

Additional Coverage Considerations

Standard homeowners insurance policies may not cover:

- Flood damage

- Earthquake damage

- Sewer backup

- Certain high-value items

Homeowners should evaluate whether supplemental coverage is necessary based on local risks.

Life Insurance by State

Understanding Life Insurance Options

Life insurance helps protect loved ones financially after a policyholder’s death.

The two primary categories include:

Term Life Insurance

Term policies provide coverage for a specific period such as:

- 10 years

- 20 years

- 30 years

These policies typically offer affordable premiums and substantial death benefits.

Permanent Life Insurance

Permanent policies include:

- Whole Life Insurance

- Universal Life Insurance

- Variable Life Insurance

These products generally provide lifelong coverage and may accumulate cash value.

State Regulations and Consumer Protections

While life insurance products are available nationwide, states regulate:

- Licensing requirements

- Policy disclosures

- Consumer rights

- Replacement regulations

Consumers should review state insurance department resources before purchasing coverage.

Average Life Insurance Costs

Life insurance rates depend largely on:

- Age

- Health status

- Smoking history

- Coverage amount

- Policy type

Younger and healthier applicants generally qualify for significantly lower premiums.

Shopping among multiple insurers can help consumers find more competitive rates.

Comparing Insurance Costs Across States

One of the most important lessons consumers learn is that insurance shopping should never be a one-time activity.

Rates change frequently because of:

- Inflation

- Claims trends

- Regulatory changes

- Economic conditions

- Natural disasters

A policy that was competitive two years ago may no longer provide the best value today.

Consumers should compare insurance quotes annually for:

- Auto insurance

- Health insurance

- Home insurance

- Life insurance

This simple practice can often lead to substantial savings.

Tips for Choosing the Right Insurance Coverage

When evaluating insurance plans, focus on more than just price.

Consider:

Financial Strength

Choose insurers with strong financial ratings and long-term stability.

Customer Service

Review customer satisfaction scores and claims-handling reputation.

Coverage Limits

Ensure limits adequately protect your assets and financial obligations.

Deductibles

Balance affordable premiums with manageable out-of-pocket costs.

Policy Exclusions

Carefully review exclusions and limitations before purchasing coverage.

The Future of Insurance in America

Technology continues transforming the insurance industry nationwide.

Emerging trends include:

- Artificial intelligence underwriting

- Usage-based auto insurance

- Digital claims processing

- Personalized pricing models

- Predictive risk analytics

Consumers can expect greater transparency, faster service, and increasingly customized coverage options in the coming years.

Final Thoughts

Insurance laws, coverage options, and premium costs vary considerably across the United States. Whether you’re searching for affordable auto insurance, comprehensive health coverage, reliable homeowners insurance, or long-term life insurance protection, understanding state-specific regulations and real-world pricing can help you make informed decisions.

By comparing plans regularly, understanding local insurance laws, and evaluating coverage needs carefully, consumers can secure better protection while maximizing value. Staying informed about state-by-state insurance differences remains one of the smartest ways to reduce financial risk and protect what matters most.

Leave a Reply