Introduction

Insurance in the United States is not a one-size-fits-all system. Instead, it is heavily influenced by state-by-state regulations, pricing laws, and coverage requirements. Whether you are buying auto insurance, health insurance, homeowners insurance, or life insurance, your location can significantly affect your premiums, benefits, and legal protections.

This comprehensive guide explains how insurance plans, laws, and real-world costs vary across U.S. states, helping consumers understand what to expect in 2026.

Why Insurance Varies by State

Insurance in the U.S. is regulated primarily at the state level. This means each state has its own rules regarding:

- Minimum coverage requirements

- Pricing regulations

- Consumer protection laws

- Insurance company licensing

- Risk assessment factors

Because of these differences, the same insurance policy can cost significantly more—or less—depending on where you live.

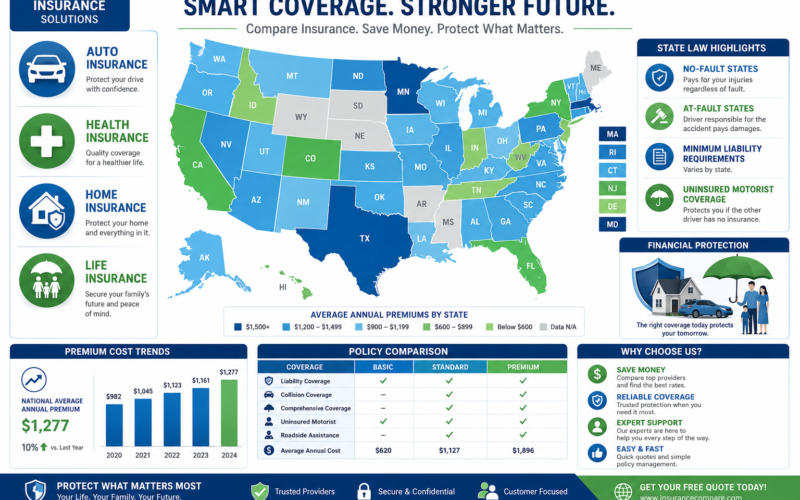

Auto Insurance by State

Minimum Coverage Requirements

Each state sets its own minimum auto insurance requirements. For example:

- Some states require only liability coverage

- Others require uninsured/underinsured motorist protection

- A few states require personal injury protection (PIP)

These differences impact both cost and coverage quality.

Real-World Auto Insurance Costs

Auto insurance premiums vary widely:

- Low-cost states: typically rural areas with fewer accidents

- High-cost states: densely populated states with higher traffic and claim rates

Key factors affecting auto insurance prices include:

- Traffic density

- Accident statistics

- Weather risks (hurricanes, snowstorms)

- Legal environments (lawsuit frequency)

No-Fault vs At-Fault States

Some states operate under no-fault insurance laws, meaning your own insurance pays for injuries regardless of who caused the accident. Others use at-fault systems, where the responsible driver pays damages.

This legal difference directly impacts:

- Claim processes

- Premium costs

- Litigation rates

Health Insurance by State

State vs Federal Marketplaces

Health insurance in the U.S. can be purchased through:

- Federal marketplace (HealthCare.gov)

- State-based exchanges

Some states manage their own healthcare marketplaces, offering additional subsidies or plan options.

Medicaid Expansion Differences

Not all states expanded Medicaid under federal guidelines. This creates significant differences in:

- Eligibility requirements

- Coverage availability for low-income individuals

- State funding structures

Real-World Health Insurance Costs

Health insurance costs vary based on:

- Age

- Income level

- Location

- Plan type (Bronze, Silver, Gold, Platinum)

Urban states with higher healthcare costs generally have higher premiums.

Home Insurance by State

Risk-Based Pricing

Homeowners insurance is heavily influenced by geographic risk factors such as:

- Hurricanes (Florida, Gulf Coast states)

- Wildfires (California, Western states)

- Tornadoes (Midwest states)

- Flooding (coastal and river regions)

Higher risk areas typically face higher premiums or stricter coverage rules.

Coverage Types

Standard home insurance policies include:

- Dwelling coverage

- Personal property protection

- Liability coverage

- Additional living expenses (ALE)

However, some natural disasters like floods or earthquakes often require separate policies.

Real-World Home Insurance Costs

Costs vary dramatically depending on:

- Property value

- Construction type

- Local disaster risk

- Insurance claim history in the area

For example, coastal homes may pay several times more than inland properties.

Life Insurance by State

Regulation Differences

Life insurance is generally more standardized nationwide, but state regulations still affect:

- Policy approval rules

- Consumer protections

- Tax treatment of benefits

- Insurance company operations

Types of Life Insurance

Common life insurance options include:

- Term life insurance

- Whole life insurance

- Universal life insurance

Each type offers different long-term financial planning benefits.

Real-World Life Insurance Costs

Life insurance premiums depend on:

- Age

- Health condition

- Lifestyle (smoking, occupation risk)

- Coverage amount

- State-level underwriting regulations

Some states with higher living costs may also have slightly higher premiums.

How State Laws Affect Insurance Pricing

State regulations influence insurance pricing through:

1. Tort Laws

States with higher litigation rates tend to have higher insurance premiums.

2. Rate Approval Systems

Some states require government approval for premium increases, while others allow more flexible pricing.

3. Risk Pool Distribution

Insurance companies calculate risk differently depending on statewide loss statistics.

4. Consumer Protection Laws

Stricter regulations often lead to more stable but sometimes higher premiums.

Comparing Insurance Costs Across States

Here is a general breakdown:

High-Cost Insurance States

- California

- New York

- Florida

- Louisiana

Moderate-Cost States

- Texas

- Illinois

- Washington

- Georgia

Lower-Cost States

- Iowa

- Idaho

- Vermont

- Nebraska

These differences reflect population density, weather risk, and legal environments.

Tips for Choosing Insurance by State

1. Understand Local Requirements

Each state has unique minimum coverage laws.

2. Compare Multiple Providers

Rates can vary significantly between insurers in the same state.

3. Evaluate Risk Factors

Consider weather risks, crime rates, and traffic conditions.

4. Bundle Policies

Combining auto, home, and life insurance often reduces total cost.

5. Review State Insurance Departments

Most states provide official insurance comparison tools and consumer guides.

The Future of State-Based Insurance Systems

In 2026, insurance systems across the U.S. are evolving due to:

- Climate change increasing disaster-related claims

- AI-driven underwriting models

- Digital-first insurance platforms

- More flexible state-level regulations

- Rising healthcare and housing costs

These trends will continue to widen the differences between states.

Conclusion

Insurance in the United States is deeply influenced by state-by-state laws, risks, and pricing structures. Whether you are shopping for auto, health, home, or life insurance, understanding local regulations is essential to finding the best coverage at the best price.

By comparing policies carefully and understanding regional differences, consumers can make smarter financial decisions and avoid overpaying for coverage.

In 2026, the key to saving on insurance is simple: know your state, know your risks, and compare your options wisely.

Leave a Reply