Introduction: Why Insurance Varies by State in the U.S.

Insurance in the United States is not regulated at a single national level. Instead, each state has its own insurance laws, pricing rules, minimum coverage requirements, and consumer protections. This means that the cost and structure of auto, health, home, and life insurance can vary significantly depending on where you live.

Understanding these differences is essential for making informed financial decisions. A driver in California may pay very different auto insurance premiums compared to someone in Texas. Similarly, homeowners in Florida face different risks and costs than those in Ohio due to climate, regulations, and risk exposure.

This guide provides a comprehensive overview of how insurance works across states, what affects pricing, and what consumers should expect in real-world costs.

1. Auto Insurance by State: Laws, Coverage, and Costs

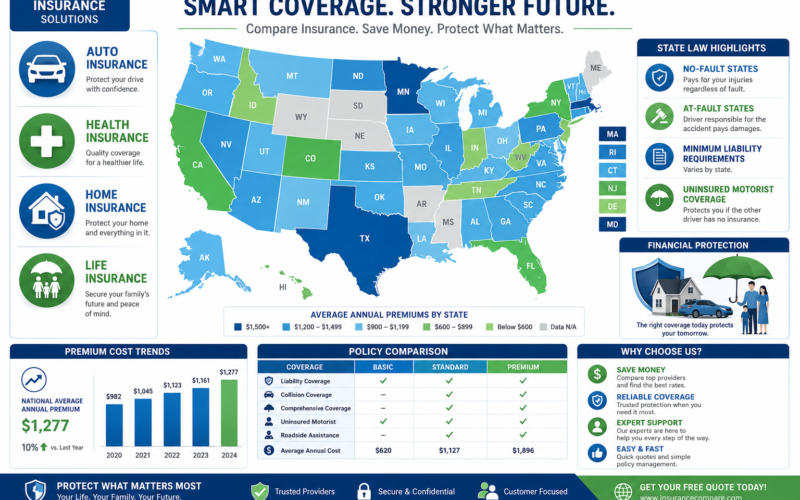

Auto insurance is required in almost every U.S. state, but minimum coverage requirements vary widely.

State Law Differences

Each state sets its own minimum liability requirements. For example:

- Some states require higher bodily injury coverage

- Others only mandate basic liability insurance

- A few states allow limited alternatives like proof of financial responsibility

No-Fault vs At-Fault States

- No-fault states require drivers to use their own insurance first for medical claims.

- At-fault states hold the responsible driver liable for damages.

No-fault states often have higher premiums due to increased claim frequency.

Real-World Cost Differences

Auto insurance costs depend heavily on:

- Population density

- Accident rates

- Weather risks

- Legal environment

For example:

- Urban states tend to have higher premiums

- Rural states generally have lower average costs

Key Takeaway

Your zip code can significantly impact your auto insurance premium—even more than your driving record in some cases.

2. Health Insurance by State: Regulations and Pricing

Health insurance in the U.S. is influenced by both federal programs and state-level regulations.

Marketplace Differences

Under the Affordable Care Act (ACA), each state may:

- Operate its own insurance marketplace

- Or use the federal marketplace

States that run their own exchanges often have more plan variety and consumer protections.

Medicaid Expansion

One of the biggest differences between states is Medicaid expansion:

- Expansion states offer coverage to more low-income residents

- Non-expansion states have stricter eligibility rules

Cost Variations

Health insurance premiums vary based on:

- State healthcare costs

- Hospital pricing

- Provider competition

- Population health risks

For example, states with higher medical service costs tend to have higher premiums.

Key Insight

Where you live directly affects your access to affordable healthcare coverage and subsidies.

3. Home Insurance by State: Risk and Weather Matter Most

Homeowners insurance is heavily influenced by environmental and geographic risk factors.

Major State-Level Risk Factors

- Hurricanes (Florida, Louisiana, Texas)

- Wildfires (California, Colorado)

- Tornadoes (Midwest states)

- Flooding (coastal regions)

Coverage Requirements

While not legally required, home insurance is usually mandatory if you have a mortgage.

Standard policies typically include:

- Dwelling coverage

- Personal property protection

- Liability coverage

- Additional living expenses

Real-World Cost Differences

Home insurance premiums vary dramatically:

- High-risk disaster states often pay 2–3x more than low-risk states

- Reinsurance costs also influence premiums

Key Takeaway

Natural disaster exposure is the single biggest driver of home insurance cost differences across states.

4. Life Insurance by State: Regulation and Pricing Factors

Life insurance is more standardized than auto or home insurance, but state regulations still influence pricing and availability.

State Insurance Department Rules

Each state regulates:

- Policy approval

- Consumer protections

- Claim dispute processes

Pricing Factors

Life insurance costs depend more on individuals than location, but state factors still matter:

- Healthcare access

- Average life expectancy

- Regulatory overhead

Term vs Whole Life Differences

- Term life insurance is generally more affordable and widely used

- Whole life insurance includes investment components and higher premiums

Key Insight

Even though life insurance is less location-sensitive, regulatory differences still impact pricing and underwriting standards.

5. Why Insurance Costs Vary So Much Between States

Insurance pricing is based on risk pools. Each state represents a different risk environment.

Key Cost Drivers:

- Weather and climate risks

- Traffic density and accident rates

- Healthcare pricing systems

- Legal environments (lawsuit frequency)

- Fraud rates and claim history

- Population demographics

States with higher risk exposure naturally have higher premiums across all insurance types.

6. Average Insurance Cost Comparison (General Overview)

While exact numbers vary annually, general trends look like this:

- Auto insurance: Highest in urban/high-traffic states

- Health insurance: Highest in states with expensive healthcare systems

- Home insurance: Highest in disaster-prone coastal and wildfire regions

- Life insurance: More stable nationwide but influenced by underwriting rules

Understanding these patterns helps consumers anticipate costs before relocating or choosing coverage.

7. How to Lower Insurance Costs in Any State

Regardless of where you live, you can reduce insurance costs by:

1. Bundling Policies

Combining auto, home, and life insurance often reduces total premiums.

2. Increasing Deductibles

Higher deductibles usually mean lower monthly payments.

3. Maintaining Good Credit

Many insurers use credit-based insurance scores.

4. Comparing Multiple Providers

Rates vary significantly between companies.

5. Reducing Risk Factors

Examples include:

- Safe driving habits

- Home safety improvements

- Avoiding high-risk claims

Conclusion: Location Matters More Than Most People Think

Insurance in the United States is deeply influenced by state laws, environmental risks, and regional cost structures. Whether you are buying auto, health, home, or life insurance, your location plays a major role in how much you pay and what coverage you receive.

By understanding state-by-state differences, consumers can make smarter financial decisions, avoid overpaying, and choose policies that truly match their needs.

Leave a Reply